Ultimate guide on opening business bank account online

Among the long list of things you need to do when setting up your business in the US, is the act of opening a business bank account. Your business bank account is going to be the hub of all your business financial transactions, your profits, your accounts payable, your employee payroll, and so much more. It is the brick and mortar of your business.

Whether you need one or not, by law, would depend on the nature of your business and the laws of your country. But, it is always recommended that you have one. To open a business bank account is not as daunting as it seems, even if it is a small business bank account.

What is business bank account?

Business bank accounts go by many names. They may be called corporate bank accounts, or company bank accounts. They all mean the same thing, though.

A business bank account is a dedicated account for your business. It is where your company’s money is managed. Your other payments are also managed from here. This could range from payables to employee payrolls and credit repayments.

A business account may be a checking account or a savings account, similar to the options available for a personal account. But it does the crucial job of keeping your payments separate from your company’s transactions. Additionally, business bank accounts come with a range of benefits (from the time of opening a business account to using the corporate account).

Which bank account and bank you opt for will depend on your specific needs, while it's also worth considering business bank account alternatives to see if they offer advantages that better align with your business model.

However, it is important to note that no matter how small your business is, it is always a great idea to open a business bank account. Many financial institutions have extra support for small business bank accounts, with dedicated benefits for SME business accounts. So, there is no such thing as opening a corporate bank account “too early”.

What to consider when opening business account

Provided below are the factors to consider when choosing a business account in order to have a seamless and effective account opening experience.

Accessibility

A business bank account is not just accessed by the person whose name is on the papers. Your finance department, accountants, compliance officers, and even some employees will need access to the bank’s facilities for smooth operations.

A banking system that has a robust and easy-to-use web portal is always a good idea. Additionally, ensure that the digital business account also has a mobile app, which allows employees to access important information and perform tasks even when they are on the move or working remotely.

Fees

There are fees often associated with opening a business account. These might be transactional fees, international currency exchange fees, or even fees for not maintaining a minimum balance.

If you are trying to optimize your business to run on as little collateral spending as possible, then opt for a bank that has the best fees offers, and the lowest fees. Also, check if there are any conditions for fee waivers that your business might be applicable for getting to operate a free business bank account is always ideal.

Transaction rules

A business bank account comes with many benefits - and these benefits are provided on the assurance that you will utilize your bank account. Your business bank savings account might have certain deposit limits that need to be met.

If you have chosen a business checking account, then there might be a minimum and a maximum number of transactions (or transactional amount) that needs to take place. Carefully go over the transaction rules for your account opening options before deciding which one to go with.

Additional features and benefits

Financial institutions recognize the importance of providing as many benefits to companies as possible. A lot of added benefits are available to business bank account owners, particularly if you open an SME bank account.

These can range from accounting integrations and collateral-free corporate cards to better interest rates and spend analysis tools. Take a thorough look at what range of features and benefits your bank offers to companies that open an account with them.

Account opening process

Long processing times and truckloads of documentation is an extremely outdated practices. Banking systems today have very well-regulated and streamlined processes for businesses to open their corporate accounts.

When considering where to open a corporate account, make note of which of your options have the best process to set up a business bank account. Also, see if you have all the verification documents needed to open the account.

Balance and spend requirements

Many bank accounts have a minimum deposit amount that needs to be fulfilled when the account is opened. There might also be a minimum balance you need to maintain without incurring penalties.

This is not just limited to incoming money, though. Depending on your account, some banks also have a minimum spend requirement for the account. If your business is starting with a lower cash flow, opt for a bank that has lower requirements and a smaller nominal fee.

Requirements to open business bank account

1. Brand and company certifications

If your company’s registered name and the branded name are different, then some banks and local laws require a “doing business as” certificate. Your bank will need this, particularly if your company has multiple sub-brands.

2. Credit score information

If your business has an existing credit score, then this will be part of your application. In the situation that you are freshly opening an account during business establishment, then the account owner’s (the business owner) credit score might be required.

3. Personal identification

The business owner needs to provide personal identification to open an account in their name. The form of ID will depend on your country of residence & country of operations, but it will need to be a government-issued identification that is not expired.

4. Business registration documentation

This is the documentation that proves your business entity is registered with the authorities. It could be a tax certificate, an LLC registration document, as well as proof of office space purchase (if your business has an offline office). Your bank will need this to ensure that you are a legitimate business trying to open a corporate account.

5. Ownership and partnership agreements

The best business bank accounts make room for your business to grow and expand. This includes partnerships. If you share your business with other entities or have entities with a controlling amount of shares, then that legal paperwork is required by your bank. This is purely to ascertain how will be controlling the funds and making authorizations.

6. Licensing information

Is your business licensed? This, of course, depends on the industry that you are working in, and the country of headquarters. Some licenses are specialized and need to be obtained after you have an account. But some licenses need to be obtained on registration of your company. These licenses need to be provided at the time of opening your business bank account.

7. Employer registration information

Some countries require business owners to register themselves as such, to obtain employment rights. If you happen to live in a place with such requirements, then you will need to register yourself as an employer and provide this documentation at the time of opening a business bank account. It is also important to keep handy your social security number or government-issued personal identification number.

Streamline your financial processes with Volopay's business account

Steps to opening a corporate bank account

Do your research

Take a thorough look at all possible offers, benefits, and fees before choosing a bank. When you are opening a corporate bank account, it is important to do research pertaining to your current situation and where you see your business growing in the future.

Decide which bank you will opt for

Once you have decided which bank you want to open an account with, look into every option available with them. If you can speak to a bank representative, all the better.

Decide the type of account you will open

Decide if you will start with opening a business checking account or a business savings account (or both). Remember to look at the interest rates and charges associated with each.

Gather the required documentation

Once you know which type of account you want, make a list of all the required documents. Obtain them well in advance so that there are no surprises or delays after you have submitted your application.

You can also refer our article on what do you need to open a business bank account for a detailed guide on the documents required and process to open a business account easily.

Fill out the application

Fill out the application thoroughly and carefully. Be as detailed as possible, and provide accurate information. Your bank will process everything faster if your data is correct.

Deposit the required amount

As with most accounts (especially savings), there needs to be a nominal deposit made to open the account. Gather the funds for this and write the check that meets these nominal requirements.

Activate your bank account

Once you receive confirmation that your account has been opened, your work is not done. You need to activate your account by using it. Go ahead and familiarize yourself with the banking services (online and offline), and start using your account!

What are business banking fees and charges to consider?

Administration fee

This is the operative fee your bank charges for owning the account. It might be charged monthly or annually.

Cash payments

Cash deposits and withdrawals from the account might have charges (as well as charges for ATM usage).

Automated payments

Some banks charge for pre-approved payments or recurring transactions. Check with your bank if this is the case.

Manual payments or checks

Check processing and manual deposits also can cost money. Take a look at these fees in advance.

Minimum balance charges

Savings accounts might charge a fee if you go below the minimum balance requirement. Make sure this fee is affordable, especially if your business has a slower cash flow. It's important to keep track of your balance to avoid unexpected charges that could impact your financial situation.

Overdrafts

Does your checking and credit account allow for overdraft protection? Are you allowed to swipe into a negative balance? Sometimes recurring payments can easily send you into an overdraft. Make sure your overdraft fees are not staggering.

Additional services

Some additional services, such as specialized cards, insurance, upgrades, advisories, and report generation, can be charged as premium services. To open a low-cost or free corporate account, be sure to ask your bank if these services need to be paid for separately.

International transactions

International transaction fees can be broken down further into exchange rates, receiving bank charges, administrative fees for the wire transfer service, etc. Get a good idea of how expensive it can be to send or receive money from a different country (particularly if you frequently pay for it).

Benefits of having business bank account

The primary benefit of opening a corporate account is to separate your personal and business finances. Your payroll and household expenses don’t need to be mixed. Everything pertaining to your business is handled separately, and can also be analyzed separately. Credit scores are also separated so that your personal creditworthiness does not impact your business (or vice versa).

Accepting payments to a personal account can be tricky. Sometimes it needs to be an NEFT/SWIFT transfer, or through a payment application. But many of your clients and customers might need to make card payments to you. A corporate account lets you accept debit and credit card payments, which not only expands your market but also makes your customers’ lives easier.

From a brand reputation perspective, having a business bank account can improve your credibility. Customers are more likely to make payments to an account that is registered as a legitimate business, instead of a personal account. Employees’ salary slips and payroll make their tax filing streamlined. Additionally, all invoices, receipts, and reports can be generated in the name of your business.

Having a corporate bank account creates a very clean and transparent money trail for your business. This comes in handy for compliance, audits, and also when applying for loans and investors. Having a no-nonsense record of your company’s payments improves your legitimacy as a business.

A corporate bank account lets you share the account with your partners and employees without having to hand over any personal assets. Everything related to your company’s finance can be easily accessed by authorized people, and you can have a transparent system for efficient business transactions.

When should you open business bank account?

Most important thing to keep in mind

It's never too early to open a business bank account. As soon as you have registered your business and obtained the necessary licenses, you can open an account. Some specialized licenses might even require you to have such an account. You also will need a business account if you are entering into any kind of partnership.

Getting started early ensures that your audit trail is clear from the very beginning. Many banks have bundles and offers for smaller businesses, so you don’t need to worry about being a unicorn to open such an account. Just remember - if you are looking to scale your business, then your financial institution of choice should have the room for your account to grow profitably.

Why Volopay is the best business account?

Volopay is not a bank. It is better than a bank because it offers all the benefits of a business bank account, while also offering a wider range of services and possibilities.

Bill Pay

Volopay’s Bill Pay features work better than a bank account. A centralized location for all your finances eliminates the need for multiple bank accounts in different locations. Regardless of where your company is located or how many branches it has, your business can access an eagle-eye view of all its funds from a singular interface.

Moreover, the Bill Pay feature allows you to make a variety of payments at the lowest possible fees. International transactions occur at competitive exchange rates, with significantly lower charges compared to wire transfers (and lesser time!). Your company policies can be assigned to transactions to manage accounts payable in compliance with audit requirements. Budgets can be applied to different departments. It is a one-stop shop for your business banking needs.

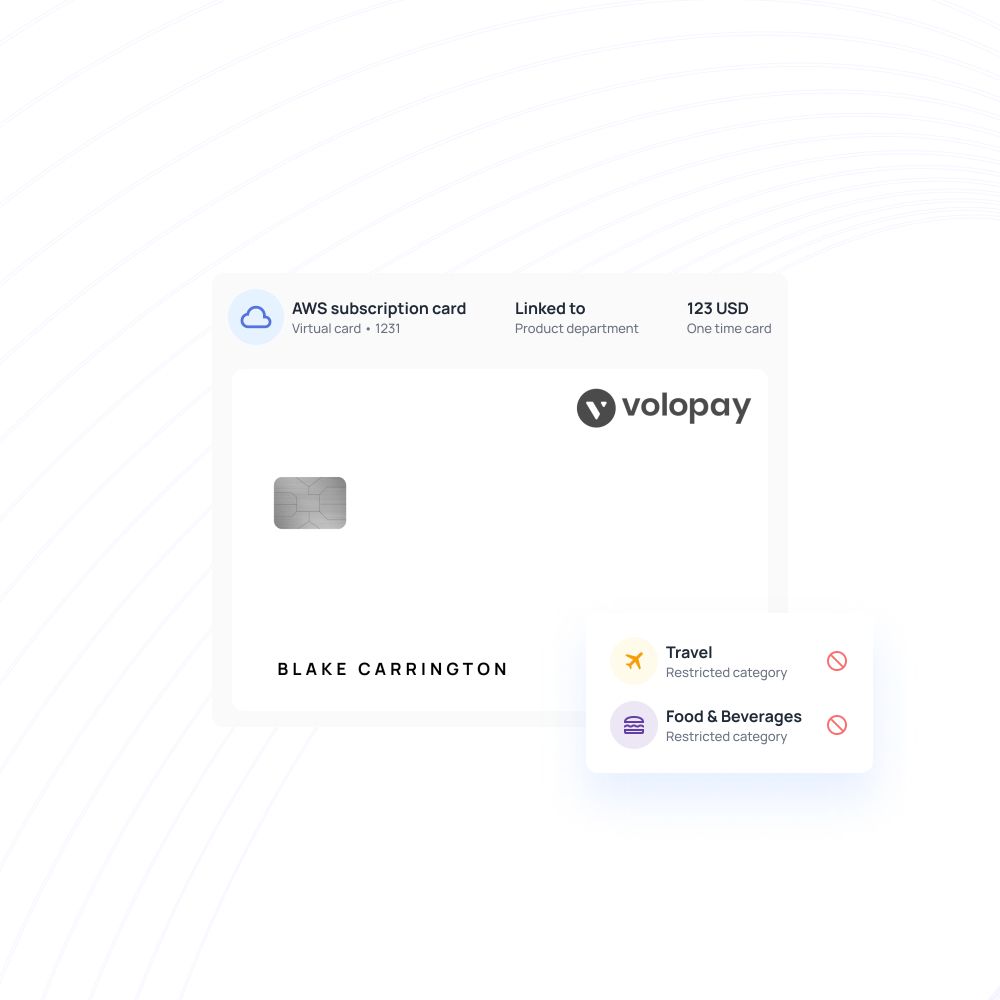

Virtual & physical cards

Instead of giving your employees access to a plethora of debit cards, you can give them corporate cards with Volopay. They are far more secure and protected from fraud. You can give your employees physical cards if they frequently make offline payments - and an unlimited number of virtual cards for online transactions.

If your business needs to make SaaS payments, or other recurring payments, these virtual cards can be used for vendor-specific payments.

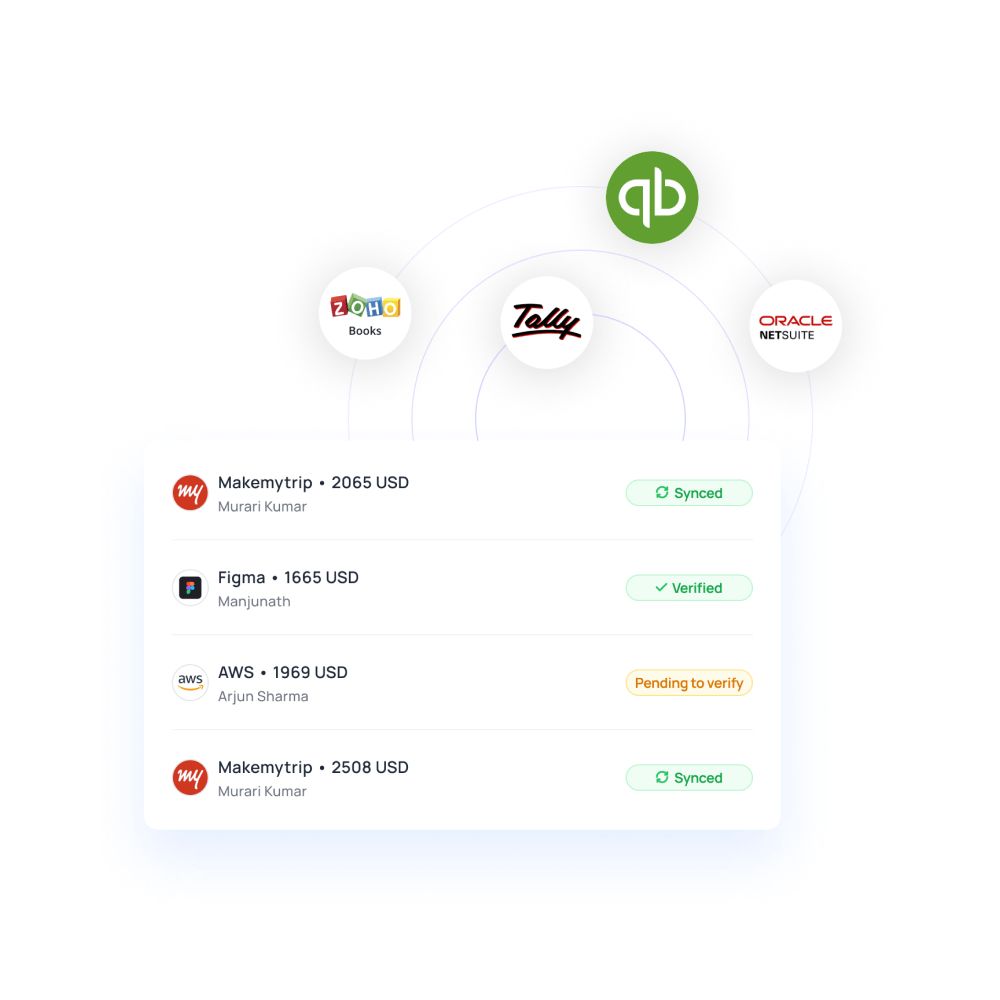

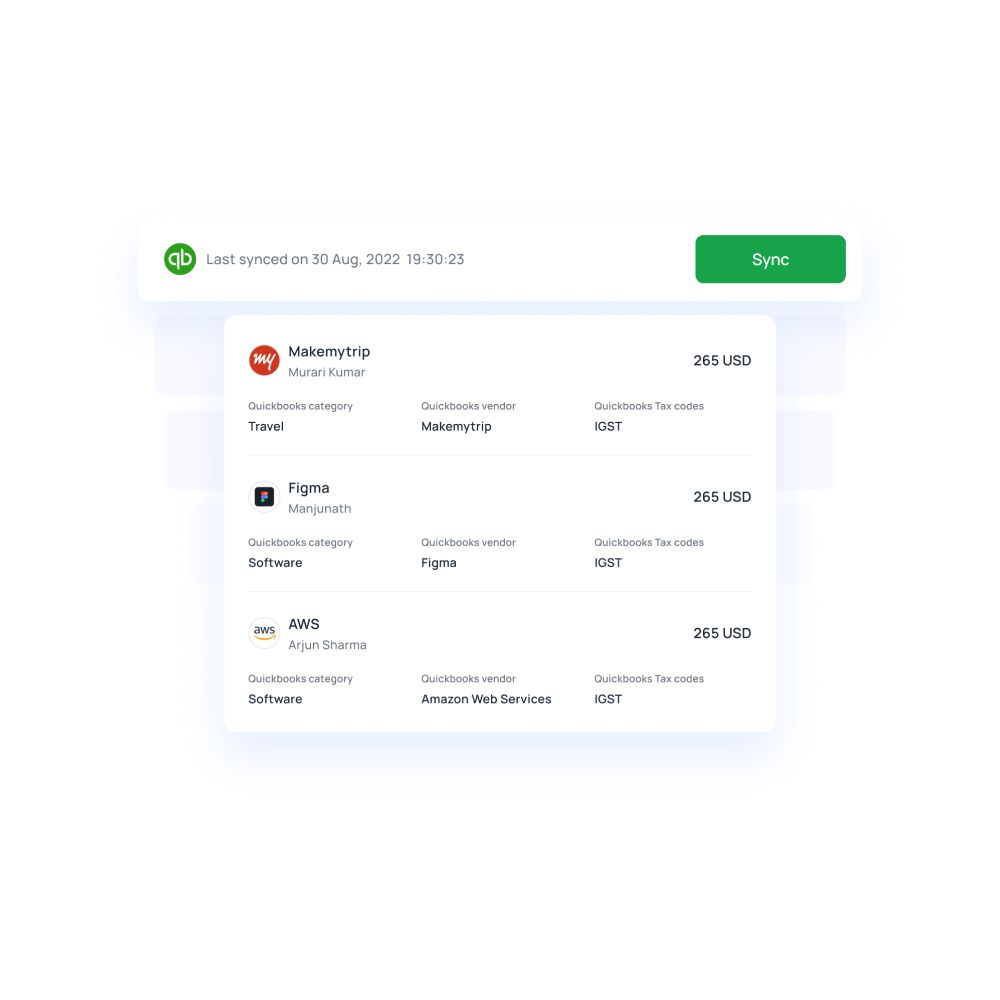

Accounting and HR integrations

Even if you choose an excellent banking plan, there are high chances that it may not come with accounting integrations. The automation of accounting has become vital for businesses and having to externally download data only makes the process more cumbersome.

Volopay allows you to integrate your accounting software directly with the portal so that data is transferred directly without manual entry. Volopay also integrates with some HR software that manages payroll payments.

Real time access

Since Volopay is software, everything takes place in real-time. If an employee requests reimbursements, pays a vendor or swipes a card - all data is updated as these transactions take place.

The ability to give all your employees accounts also means that multiple people can access this information, analyze data, and generate reports in a collaborative and streamlined manner. Volopay also has a mobile app so that employees can view their accounts on the move.

FAQs

On the surface, they function the same way. But a corporate account has functionalities specific to a business, unlike a traditional bank account. A corporate account can have offerings such as debit cards for employees, more lucrative interest rates, and payroll processing services. The balance requirements and fees are also, overall, better for your business.

The purpose of a business bank account is to have all your business-related transactions in one place. It separates all personal and business payments. Additionally, business accounts have certain benefits that do not apply to personal accounts (benefits that depend on the bank you choose).

No, opening a business bank account will not affect your personal credit score. However, if you avail of credit facilities, then your business credit score will be calculated separately.

The process of setting up your Volopay account is fairly quick and simple. Once you’ve signed up for a plan and provided your documentation (KYB documentation for verification purposes), you will be invited to create an administrative account. You can get started immediately after that.

Business checking accounts do not, but a business savings account does earn interest. The interest rate depends on the bank you use, and the tier of the account you open.

Volopay is not a bank. It is a spend management platform that allows you to access a requested credit line, create physical & virtual corporate cards, and handle all your SWIFT & non-SWIFT payable transactions. Your funds are stored in an account with ANZ. Volopay is the software that you use to access and utilize your funds, while also managing them without the need for multiple accounts in multiple countries.

Extremely so. Volopay does not keep your money in its own pocket. Your funds are stored in an ANZ bank account, which is in compliance with ASIC (Australian Securities & Investments Commission). Your data is protected with bank-grade security encryption and access protocols.

Volopay only charges a subscription fee for its software, and there is a range of plans to choose from. If you opt for a credit line with Volopay, there is a nominal fee for that.

All transactional fees (such as currency conversion, administration fees, bank markup fees) are charged by banks, depending on the country to which the payment is being made and the country in which your business is located. This fee is not charged by Volopay.

Trusted by finance teams at startups to enterprises.