How to build business credit in 10 simple ways?

Building strong business credit can favor you in many ways, from improving your bank loan eligibility to securing low-interest rates. This score is the identity of your business's financial position and stability and how credible you are in repaying the remittance. It also shows the smart management of the cash flow of your business.

Due to negligence or lack of awareness about business credit, many new entrepreneurs commit mistakes and make wrong financial decisions that call forth nasty or adverse credit. As a new business, it’s indispensable to build business credit by following the appropriate financial practices.

What is business credit?

A business credit score is exactly like a personal credit score but is granted for businesses. With this number, one can identify your business's credibility when repaying bank debts or money borrowed from other sources.

A typical business credit score can range anywhere from 0 to 100. Factors like company size, how long the debts are owed, past credit history are used to estimate the business credit. Before a lender loan, they need a guaranteed factor to determine whether a company is eligible to repay the amount with interest. The score also manifests maximum borrowing capacity and time taken for repayment.

Why does business credit matter?

Your business credit score matters to you when you need exterior financial support to run your business. The score can prove your creditworthiness and get you better deals on interest rates or move the loan amount limit needle to your preference. It also affects when you try to attract investors to invest in your business.

Like a domino effect, when you receive a loan with high-interest rates, it will take longer to pay them off. And this is strong enough to disrupt your cash flow and further impact an already low score.

As a personification of your current financial strength, it is pretty important to maintain a good business credit score and, if not, build business credit from scratch.

What is importance of building business credit?

Good business credit makes it quicker and easier to obtain business financing

When you’re applying for business loans a good business credit score is helpful because it quickly solves cash flow problems. Lenders tend to check your business credit score when you apply for financing. A business credit score that is in higher ranges will significantly boost the profitability of approval for any application you make for business lines of credit, small business loans, or other business financing products. A good business credit score is essentially an indicator to lenders that the business in question is capable of making repayments on time.

Improved credit and repayment terms with suppliers and vendors

You should focus on how to build business credit because a positive score enables improved chances of obtaining trade credit and better repayment terms from suppliers and vendors. A good business credit score portrays your business as a client that is trustworthy. This means you will have better chances of getting repayment structures that are flexible.

Personal credit score stays protected

By building your business credit score you can also ensure that your personal credit score stays protected at all times. Using personal credit is a big no-no for making expenses related to your business. If your credit utilization score is high there will be a negative impact on your personal credit score.

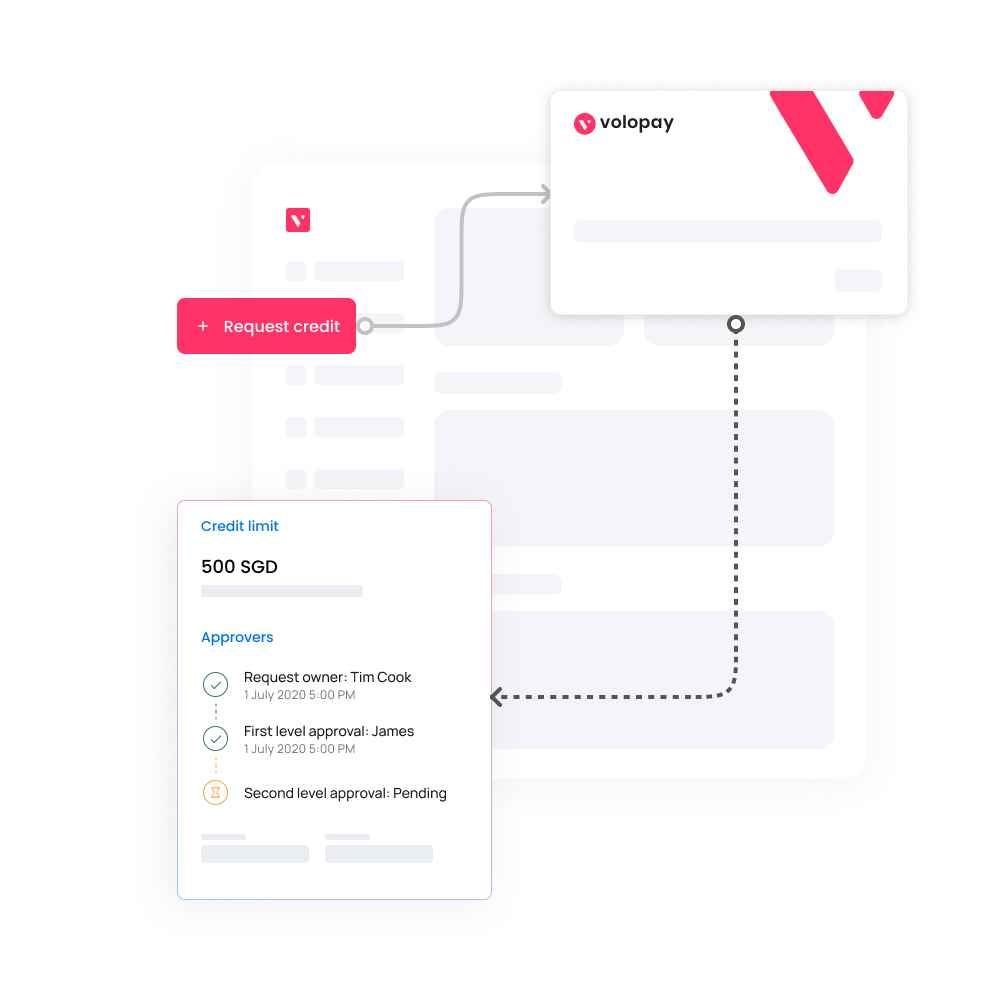

Avail flexible credit line with Volopay for your business today!

How to build business credit score?

It’s viable to get your business credit score high when you have the appropriate strategies and play them right. Here are some common techniques that have worked wonders for other businesses in building business credit.

Get employer identification number

Getting the unique identification number is probably the first step if you don’t have a business credit score.

Employer identification number in different countries:

- The United States

If your business is put up in the US region, apply for the employer identification number online from IRS (Internal Revenue Service). You are eligible to get an identification number whether you are a sole proprietor or a corporation. The online process is very simple in that it takes only a few hours.

- Australia

In Australia, this identification number for businesses is called the ‘Australian Business Number (ABN)’. The registration process is free and you can do it through the online government portal. ABN is different from ACN (Australian Company Number). Australian Company Number is for companies that are registered as separate entities.

- Singapore

In Singapore, ACRA (Accounting and Corporate Regulatory Authority of Singapore) issues UEN for local companies and businesses around the time of business registration. After choosing the entity type, businesses need to register themselves in the Bizfile portal maintained by ACRA, Singapore.

- India

If you have a business established in India, you need a unique Employer Identification Number (EIN) which is assigned by the IRS once you register your firm. It is 11 digit number also known as the Taxpayer Identification Number (TIN). The registration process can be done both online and offline.

- Indonesia

To be qualified for enlisting VAT, the Indonesia VAT regulation sets an edge of IDR 4.8 billion deals each year. All paper-based applications for VAT enlistment should be submitted to the territorial duty office of the organization. When the individual or business registers for VAT charge, a unique Tax Identification Number (NPWP) of 15 digits is allowed to them.

- Philippines

A nine-digit number used as the following number by the Internal Revenue Service (IRS) is alluded to as a Tax Identification Number (TIN). You can also register for your tax identification number (TIN) online using the BIR eRegistration portal. However, only the individuals who fall under the category of self-employed, employees, unemployed, and mixed-income earners under the Executive Order No.98 are liable to register online.

Getting an employer identification number qualifies you to get your corporate bank account, file taxes under your business identification, start building your business credit score.

Countries other than the US have their business taxpayer identification system where employers can register themselves.

Get incorporated

The next step is to register the business based on your corporate entity. If you are already a registered organization in your local jurisdiction, you can ignore this step. But if you haven’t, be aware of the terms LLP, LLC, and corp based on the business structure. Here is a short explanation of the terms.

1. LLP (Limited Liability Partnership) is almost the same as a sole proprietorship, except you have partners who sign the limited liability partnership bonds. The general partner or proprietor will most likely monitor business activities and have a significant say in them, whereas the limited partners are there only to provide financial backup.

2. LLC (Limited Liability Company) - it’s a hybrid between sole proprietorship and partnership. We mean the word hybrid because LLC can help the business owners pass-through taxation while getting the limited liability benefits of a corporation. Find the proper business structure that suits your entity and get incorporated from the state corporation.

Google my business

You must have chosen a business name around the time of the incorporation. Since you have the name, you can update your business name and location. And you can claim the business if it’s already available. Google is the primary point of the search when someone has to research a business and its credibility and performance. Before establishing the credit score, claiming the company and establishing a name must be done.

Open business bank account

Separating personal finances from business finance is a must as it can help you maintain clear records and pay taxes quickly. To begin with, you can open a business checking account with any banking services vendor in your locality.

Opening a business account can also help you when you have sudden financial difficulties and need a small loan. Having an account in the bank can play an added advantage while getting the loan approved at competitive interest rates. Even when you have a corporate credit card, you can still use your business checking account to pay back the dues.

Make your payments on time

On-time payment is a no-brainer if you are focused on building or improving your business credit score. Build and maintain the vendor credits. Whether it’s the monthly dues of a credit card, bank loan, or a vendor payment, paying it at the earliest keeps you in good books and plays a crucial role in improving your credit score.

Delayed or missed payments are unprofessional and demeaning, creating a bad reputation. It also affects the future deals that stand in line and trigger late payments charges. It’s not just the repayment but the credit utilization which affects your scores. So, use your credit card or credit line wisely and never use it up to or beyond the maximum limit allocated.

Each bureau has a different way of credit score computation. But no way you can progress towards a high credit score with a bad history of delayed and late payments. Automating and scheduling the payments beforehand is exactly how to build business credit and develop good payment practices.

Build and maintain vendor credits

Vendors can offer you big-time support in boosting your credit score. When you sign up with a vendor and purchase products/services from them, try repaying them as early as possible and building trust. Try to maintain a good relationship with them and continue to be on cordial terms as you purchase from them.

Once you gain their trust, you can earn vendor credits from them. Your vendor might have accounts with a different bureau. Check which vendors report to which agencies and work closely with them to gain recognition.

Update your information with business credit bureaus

There are different business credit bureaus whose primary function is to collect a company's financial records, analyze and compute its business credit score. As mentioned before, each bureau has its theories, formulas, methods, and regulations. Some of the well-established bureaus are Equifax, Dun & Bradstreet, Transunion, and Experien. Also, FICO is the most accurate and most used, which lenders use all the time to make loaning decisions.

Your money lenders, investors, and vendors can present in anyone. So, it’s best to get registered in all of them to get business credit scores. This way, you can get identified when they search for your score in the above systems.

Corporate credit card and business credit card

Cash flow management is a delicate thing that you must manage efficiently; otherwise, you would run out of money to keep your business moving. To regulate your cash flow and make expensing stress-free, you will need assistance from corporate credit cards. Find a vendor who has attractive plans, easy signup policies, less interest and FX rates, and more cashbacks.

Each business has different needs. To analyze the features in-depth and choose technically and financially strong ones. When you have a credit card with an assigned line of credit, you can manage your bill and vendor payments. With that card at the end of the month, you can repay them conveniently.

Some platforms offer you discounts for using credit cards too. Now using this credit card can benefit you in two ways. One, you can pay your loans and dues on time. Two, by establishing a quick credit card due to repayment strategy, you can boost your credit score too. Be aware that it can also backfire when you don’t pay the credit back on time by impacting your score negatively.

Keep your business expenses and personal expenses separately

Given the steps that have been discussed before, it’s evident that you will consider getting a business account and credit card. But it’s not too uncommon where small businesses to use their personal credit and account when they run out of cash. Whether you are in the budding stage or already established, keeping the business and personal expenses separated can set off a smooth financial journey.

Regularly monitor your business credit reports

Without knowing where you stand, you will be clueless about what, when, and how to build business credit and keep improving things. Keep reminders to frequently check your business credit reports and scores in all the bureaus you have registered at. There are also possibilities for minor computational errors, and when you don’t check, you will never get the opportunity to rectify them.

Get a hassle-free line of credit from Volopay with zero interest rate

How long will it take to build business credit?

Time taken to build business credit depends on the type of strategies you follow. According to financial experts, it can be anywhere between one year and three years. Some can achieve building a good credit score within one year too.

Though the experts' calculation states three years when a business makes slow and steady progress, still the period is too long to act on improvement strategies consistently. And then there are companies that don’t even make it to their 2nd or 3rd anniversary.

The prolonged duration can further hamper the score if the company is not ready with proper backup plans. This is why there is a need to build a foolproof business credit score plan right from the inaugural duration.

The step-by-step plan shared in the above section can be of excellent guidance. And remember that it’s always a work in progress because if you fall out of the path any time, it can take a hit on your scores.

How to maintain business credit?

What’s more challenging than just knowing how to build business credit score is maintaining the score at the same levels. Even minor disruptions are powerful enough to bring your score down to dangerous levels. Here is how you can maintain your score.

Maintain good relationships with your vendors and money lenders - Don’t give them an opportunity to send you payment reminders, or don’t position yourself in a place where you have to give excuses.

Make right financial decisions - Consider your current cash flow, savings, and pending dues before taking a big step. Pay heed to budgets and make intelligent, accurate budget plans. Also, ensure that you stick to the budget tightly.

Be on good terms with your credit card partner - Unlike the above terms, this has a direct relationship with your credit score levels. Analyze the credit line you are offered and how much you need. Be aware of how much is spent every month and when the dues are paid. Overall, maintain a warm and professional relationship and steer clear of delays and chaos.

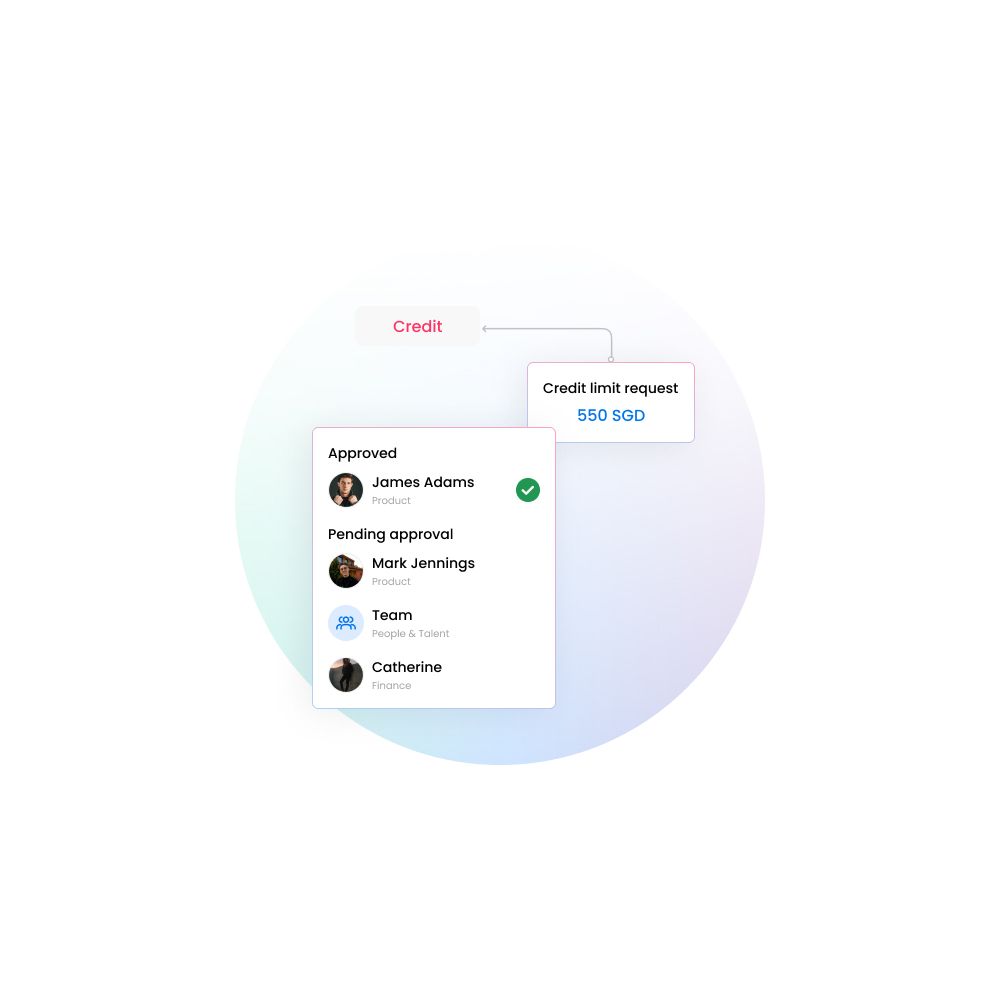

How to avail business credit line with Volopay?

Volopay understands the arduous journey you are about to embark on when you build the business credit score. So, we have introduced a wholly hassle-free and simplified process to apply for a business line of credit with Volopay.

Now manage your subscription fees, online application fees, employee travel, and business expenses seamlessly with the help of Volopay’s online credit card management platform. You can also draw the credit to make your bill payments.

Here is what you have to do to earn the line of credit to put them to use for the above reasons.

- Open Volopay’s expense management system’s dashboard.

- Go to the credit section, and you will see the option to apply for credits.

- Once we receive your request, our team will run a credit assessment and let you know the credit line you are eligible for.

- The maximum level of credit offered is SGD 500k. It varies from business to business.

- The minimum amount of documentation is required to get this entire process approved. You will be required to provide your business financial statements for the past months.

- You can request a credit line increase through the application whenever needed.

FAQs

It can take up to 3 years to build a good, positive business credit score. But with exceptional financial performance, some businesses manage to make it within one year. If new businesses focus on their credit score right from the start, in a year or two, they can reach a strong mark.

Your personal credit will not affect your business credit score as long as you have your finances separated. In order to improve your business credit, you can start with better repayment strategies. If you have pending loans, work on the repayment strategy and make payments earlier. If there are any unclear past dues, clear them right away. Organic strategies like this will help you fix your bad credit score in two to three years.

As a sole proprietor, you might manage your personal and business expenses together. In order to build your sole proprietorship business credit, register your business and get a business banking account. Manage your business expenses from this account and schedule payments on time. Once your business loan application is approved, strategize your due payments in a way that wouldn’t affect your cash flow.

Post-registration of your business, get a business banking account. Pair with vendors who report to credit organizations. Make your outgoing payments on time and maintain good relationships with your vendors. Choose your funding and repayment carefully based on your incoming cash flow. Keep track of your business credit score by registering with credit agencies like Dun&Bradstreet.

Volopay credit lines are interest-free as long you repay the borrowed amount within the end of the billing period. You can make your repayment right from the app in seconds and always see an outstanding balance.

Traditional banks require documents like your personal identification (passport, driving license), bank statements of the past 3 or 6 months, and business credit score statements. Volopay offers you a no-collateral credit line. We don’t require you to produce any collaterals to get business credit lines. Monthly statements might be needed in some cases.

Trusted by finance teams at startups to enterprises.